Short Straddle Options Strategy

A short straddle is an advanced options strategy constructed by simultaneously selling (writing) a call option and a put option for the same underlying asset, both with the same strike price and the same expiration date. This configuration creates a market-neutral position, as the trader does not anticipate a significant directional movement in the underlying asset’s price. Instead, the fundamental objective of the short straddle is to profit from a lack of volatility, specifically when the underlying asset is expected to remain relatively stable or trade within a narrow range until the options expire.

The term “neutral” in this context extends beyond merely expecting no price movement. The strategy explicitly benefits from a decrease in implied volatility over the life of the options contracts. This suggests that a trader might initiate a short straddle not just when predicting price stagnation, but more critically, when they believe implied volatility is currently inflated and is likely to contract. Therefore, the short straddle functions as much as a “short volatility” play as it does a “neutral” one, where the decline in the market’s expectation of future price swings contributes significantly to profitability.

To implement a short straddle, a trader executes two distinct yet simultaneous sell orders:

Selling a Call Option: This obligates the seller to deliver the underlying asset at the specified strike price if the option buyer chooses to exercise their right to purchase it.

Selling a Put Option: This obligates the seller to buy the underlying asset at the specified strike price if the option buyer chooses to exercise their right to sell it.

Both options are typically chosen to be “at-the-money” (ATM), meaning their strike price is very close to the current market price of the underlying asset. This selection is strategic, as ATM options generally possess the highest extrinsic value, thereby maximizing the premium collected by the seller. However, advanced traders may deviate from a perfectly ATM strike. For instance, if a subtle bullish bias is held, a trader might sell a straddle with a strike price slightly above the current underlying price. Conversely, for a bearish skew, the strike might be set slightly below the current price. This demonstrates that while the core concept is market neutrality, the “neutral” aspect can be fine-tuned. It is not always about anticipating absolute stagnation, but rather expecting the asset to remain within a specific, pre-defined range that can be strategically adjusted based on a more nuanced market perspective. This customisation adds a layer of complexity and potential for strategic adaptation beyond a purely non-directional approach.

The short straddle is ideally suited for market environments characterised by low volatility and an expectation that the underlying asset’s price will remain relatively stable or trade within a narrow range until the options expire.Traders frequently deploy this strategy when implied volatility (IV) is unusually high, as elevated IV inflates the premiums received from selling the options.This offers a larger potential profit should the options decay in value as anticipated. The ultimate objective is for both the sold call and put options to expire worthless, allowing the trader to retain the entirety of the collected premium.

The effectiveness of this strategy is deeply intertwined with the interplay of implied volatility and time decay. The strategy thrives when implied volatility is elevated at the point of entry, as this translates into higher premiums for the seller. Subsequently, the expectation is that this elevated implied volatility will decrease (a phenomenon known as volatility contraction) as time passes and the options approach expiration. This dynamic provides a dual benefit for the short straddle seller: initial high premium collection followed by the erosion of that premium due to both time decay and a reduction in market uncertainty. This highlights that the ideal scenario is not merely low realised volatility, but rather high implied volatility at entry that is then expected to decline, underscoring the critical role of volatility analysis as a primary driver for initiating this trade, rather than solely relying on a flat price forecast.

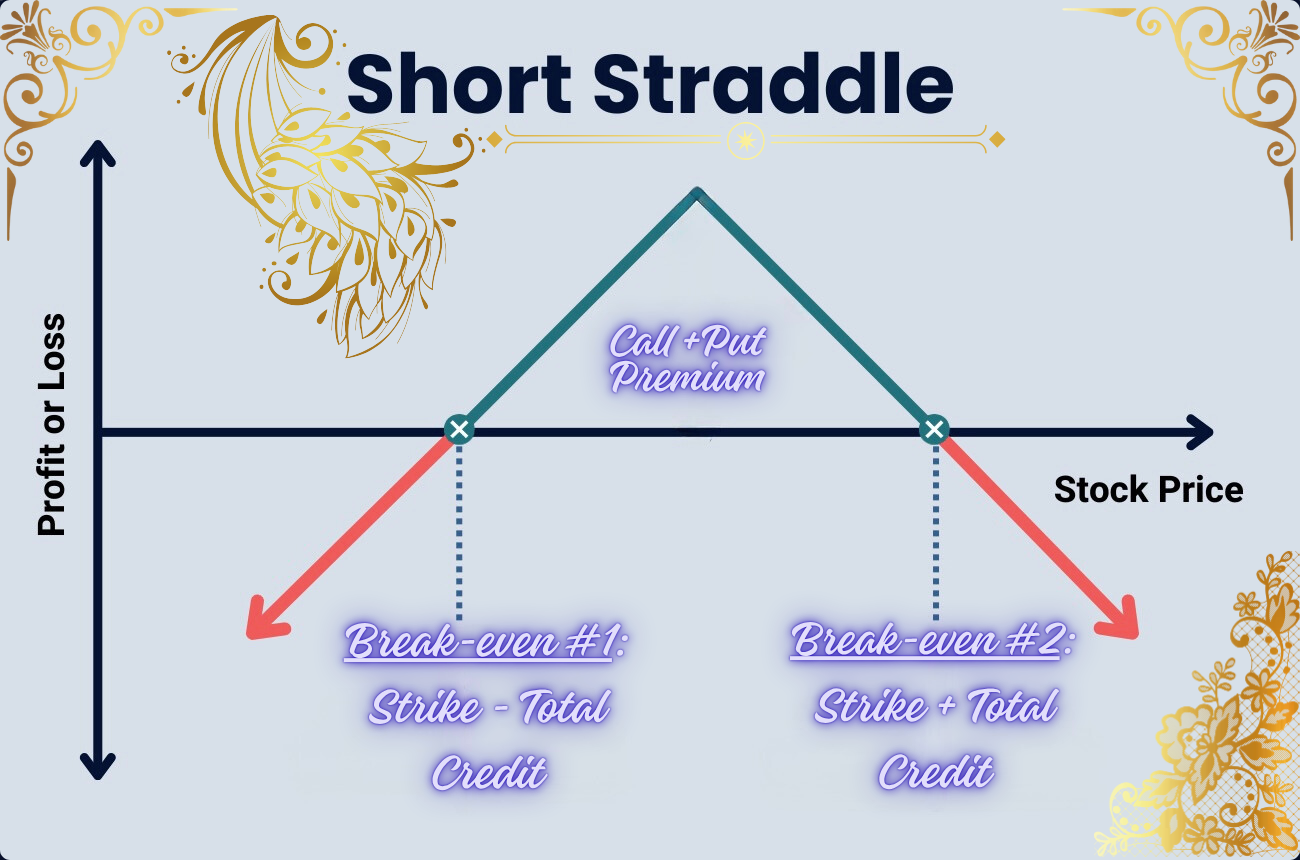

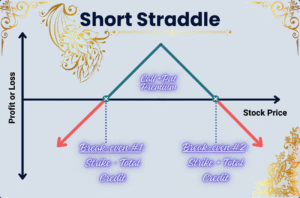

The maximum profit achievable with a short straddle is precisely limited to the total premium collected from selling both the call and the put options.This optimal outcome materializes if the underlying asset’s price at expiration is exactly at the common strike price. In this specific scenario, both the call and put options expire worthless, allowing the seller to retain the entire initial credit.

It is important to acknowledge that the probability of the underlying asset closing exactly at the strike price at expiration is exceedingly low. However, the strategy’s profitability is not entirely contingent on this precise outcome. Partial profit can still be realised if the underlying price closes between the two breakeven points. This indicates that while the theoretical maximum profit is a specific point, the practical objective for traders is often to ensure the underlying asset remains within the broader profitable range defined by the breakeven points, leveraging the ongoing time decay within that zone. Consequently, traders should focus on the overall profit zone rather than fixating on the elusive exact strike price at expiration.

A short straddle is characterized by two breakeven points, which delineate the price range within which the strategy will generate a profit. These points are calculated by adding and subtracting the total premium received from the common strike price:

Upper Breakeven Point: Strike Price + Total Premium Received

Lower Breakeven Point: Strike Price – Total Premium Received

For example, if a straddle is sold at a $60 strike price for a total premium of $7.50, the upper breakeven point would be $67.50 ($60 + $7.50), and the lower breakeven point would be $52.50 ($60 – $7.50). The strategy yields a profit if the underlying asset’s price at expiration remains strictly between these two calculated points.

These breakeven points are more than just static price levels; they function as dynamic volatility thresholds. A higher premium collected, often a direct consequence of higher implied volatility at the time of entry, effectively widens the profitable range. This means that the breakeven points directly reflect the market’s expectation of future price movement and the compensation the seller receives for assuming the associated risk. A wider breakeven range provides a greater “cushion” against adverse price movements, but it can also signify that the market perceives a higher degree of risk, demanding a larger premium in return.

The most critical characteristic and primary disadvantage of the short straddle is its theoretically unlimited maximum loss potential. This severe risk materializes if the underlying asset’s price moves significantly away from the strike price in either direction, exceeding the calculated breakeven points.

Upside Risk: If the stock price experiences a sharp increase, the short call option becomes deeply in-the-money. The seller is then obligated to deliver shares at the lower strike price. If the trader does not already own the underlying shares, they would be forced to purchase them at the much higher current market price to fulfill this obligation, leading to substantial, uncapped losses.

Downside Risk: Conversely, if the stock price plummets, the short put option becomes deeply in-the-money. The seller is then obligated to buy shares at the strike price, which could be significantly higher than the asset’s depreciated market value, resulting in considerable losses that can theoretically extend down to the underlying asset’s price reaching zero.

This inherent unbounded risk profile necessitates extreme caution and the implementation of robust risk management techniques. The strategy is typically recommended only for experienced traders who possess a deep understanding of market dynamics and the discipline to manage such exposure. The inherent paradox of this strategy is that it is designed for a “neutral” market outlook, yet it carries “unlimited loss potential”. This creates a fundamental tension: a strategy that bets on stability faces catastrophic risk from unexpected instability. The “neutral” outlook refers to the expected outcome under normal conditions, while the unlimited loss refers to the worst-case outcome resulting from an unforeseen, significant market move. This distinction underscores that “neutral” in options trading does not equate to “low risk.” Instead, it implies a specific type of risk: the risk of an unexpected, large movement away from the central price expectation. This characteristic demands a strong conviction in low volatility and comprehensive contingency planning.

Post Comment